By Chengmai Zhang

The origin of Grameen Bank

Around 1972,an economist called Muhammad Yunus was in the village of Chobra, Bangladesh. He spotted a woman who was making a bamboo stool near the school. He asked, “How much money can I make?” The woman replied, “The money is from the usurer. Only 0.5 takas can be earned by processing a bamboo stool. The income is extremely meager.”

Yunus then asked again: “If you have money, how much money can you earn for processing a bamboo stool? “The woman said she could make 3-5 taka, which is 6-10 times what they earn from processing for loan sharks.

Inspired by this phenomenon, for the following day, Professor Yunus organized a student survey and found that it was a common situation in Bangladesh’s villages or rural areas. So he took the $27 and asked the students to lend it to the 42 people. He told them to pay the money back to the lender until the product was sold, with no interest.

The women kept their word and kept their promise. Yunus was touched by the motivation and hard-working of these village women workers. He then started to think and find that the bank will only lend the money to the rich people since they can help the bank make a profit. Thus, he came up with the idea about Grameen Bank. Grameen bank will lend the money to the poor women with low interest. And this is the original wish of Grameen Bank.

In 2006, Grameen Bank won the Nobel Peace Prize due to its contribution to eradicating poverty. By the end of 2008, Grameen Bank had distributed $7.6 billion to the poor. At the end of 2017, the bank had about 2,600 branches and 9 million borrowers, with a repayment rate of 99.6 percent.

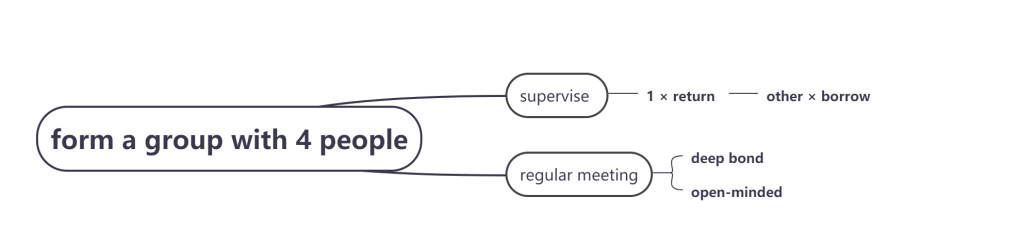

The system of how Grameen Bank works is different from that of other banks. Grameen Bank will help poor people to form a group of 4 members. They will supervise each other. If one of them doesn’t pay the money back, the rest will not have the chance to borrow money in the future.

Also, the people in the village who borrow the money will have a regular meeting to deepen the bonding between each other. The members can exchange their ideas during the session. It is a good chance for them to convey their idea and get to know each other. After this kind of meeting, members will be more open-minded. They will know that their life can be much better, and they need to do something to improve their life. It will help the poor people do their own business, get rid of poverty, and help the countryside to be more united.

Introduction of Grameen Bangladesh

Professor Muhammad Yunus began experimenting with microfinance in the village of Chittagong Chopra in Bangladesh in 1974. In 1983, the Bangladeshi government issued the Special Grameen Bank Act of 1983; thus, the world’s first bank specifically for the poor, the Grameen Bank, was born.

In 1998, Bangladesh experienced a huge flood, which caused heavy losses for Grameen Bank and millions of customers. However, the Grameen bank is not overwhelming. It began to reflect on how to improve its own rules and systems further. And in 2000, it began to change. Grameen Classic System made a significant change this time. Considering customers’ perspective to make the system more convenient, after years of repeated practice, error correction, the innovation, they formed the Grameen Generalized System. With the combined efforts of the Government of Bangladesh, the People of Bangladesh, and the Grameen Bank, the per capita income in the country increased 149% between 2008 and 2018. Rural Bangladesh has undergone dramatic changes.

There are three offices in the Grameen Bangladesh system. Branch Office is a bridge between the bank and the borrowers. Area Office is a supervision organization of the region. Zonal Office is to evaluate the region and understand the social development.

There are loads of the social impact of Grameen Bank in Bangladesh. Most importantly, Grameen bank helps women in Bangladesh. Because of the Grameen bank, the women in Bangladesh will have more money to buy food for their kids and more medicine. Also, women will exchange their ideas during the meeting. They will be more willing to make dramatic lifestyle changes such as growing more vegetables, keeping their families small, and sending their children to school for education opportunities. In conclusion, Bangladesh sets an excellent example in developing the Grameen system in a wholesome way, focusing on poverty reduction and women empowerment.

Introduction of Grameen China

In 2006, after Professor Yunus won the Nobel Prize, he visited China at the invitation of the Chinese government. Foreign Minister Li Zhaoxing and Deputy Governor Wu Xiaoling of the People’s Bank of China met with Professor Yunus in Beijing. At the same time, Professor Yunus was invited to visit Peking University and give speeches, which aroused a warm response.

In December 2014, Professor Yunus founded Grameen China in Lukou Village, Xuzhou, Jiangsu Province, marking the first implementation of the Grameen model in China. In 2019, the cooperation between China Construction Bank and Grameen China in Shenzhen was preluded. Mr. Tian Guoli, Chairman of China Construction Bank, visited Shenzhen in person and provided the first batch of 12 female customers with a small start-up capital of 8000-30,000 yuan.

In China, Grameen China mainly provides consulting services to the China Construction Bank and helps them select and manage the benefactors in the field.

The CEO of Grameen China, Gaozhan, said that since the whole system of the Grameen Bank is nearly perfect, it provides the entire system for Grameen China to study. Grameen China is standing on the shoulder of a giant. According to Zhan Gao, if there is a bank that truly understands the Grameen system and is willing to provide an opportunity, Grameen China will be flourished. Besides, in China, places like Shenzhen have many urban migrants who still can’t get credit. Despite the monetary difficulty, the poor still have unmet psychological, social needs. From these two points of view, it is still enough to realize the potential of the Grameen model in China.

Nevertheless, there are some drawbacks to develop Grameen Bank in China. First of all, Grameen China doesn’t have enough investment to get started currently. Also, according to our interview with Lee Geun(Grameen’s director of foreign cooperation), Grameen China doesn’t have the license to provide the loan based on Chinese law. Thus, even if Grameen China has enough money, it doesn’t qualify as the actual Grameen Bank in its home country. According to the Regulations on the Administration of Savings 2020, no unit or individual may handle savings deposit business except for savings institutions. Therefore, Grameen China can’t provide deposing, which is originally an essential step in the Grameen Bank system. In short, due to various institutional limits, China still has a long way to go in developing Grameen Bank.

Compare China with other countries

The Grameen China is similar to the Grameen US. They are both exist in a company form but not the bank form. However, although the two are both the company, they have considerable differences. The Grameen US is qualified to make loans and take the donation.

However, Grameen China can only provide consultation services to qualified financial institutions in China. Grameen China has no license for giving the loan. Moreover, it is also tricky for Grameen China to raise enough capital for future investment.

In addition, Grameen China is different from Grameen Bank in Bangladesh. Grameen in Bangladesh is genuinely a bank. For Grameen bank in Bangladesh, it can provide loans and provide many various services. Lee Geun said,” In Bangladesh, Grameen Bank offers 32 services, including insurance, schooling, funerals and so on. “Nonetheless, Grameen China only can work with the local bank and provides loan service.

Plus, the training process of Grameen China is different from other Grameen Bank in Bangladesh. Lee Geun said, “The large growth market in China leads to a short training period for each employee. We pay more attention to efficiency, so managers have to adapt in a short time.”

However, in Bangladesh, the training time is longer, and they have a higher requirement for employees.

Nonetheless, all the Grameen Bank that exist in our world have one similarity. They both want to help the poor to have a better life in the future. Through weekly meetings, members become more courageous in their communication. With Grameen’s help, their families’ status has risen, their children are better educated, and they have developed the habit of investing.

Based on all the information above, since all Grameen Banks have the same goal, Grameen China has loads of things to learn from other countries. The government must support the microfinance sector by developing better policies and developing infrastructure across the country. We need to establish a technical assistance fund to help potential MFIs (microfinance institutions) create appropriate products and procedures and recognize the best performance. Also, Grameen China needs to be more active in finding like-minded partners. It is essential that for them to see an institution that supports and help their work.